ACRA issues area of focus for FY2023 Financial Statements

Last updated on 7 February 2024

As part of its Financial Reporting Surveillance Programme, ACRA reviews Singapore companies’ financial statements to ensure adherence to accounting standards. ACRA recently released areas of focus to guide directors and audit committee’s as companies prepare their financial statements for financial year 2023.

Macroeconomic and geopolitical uncertainties

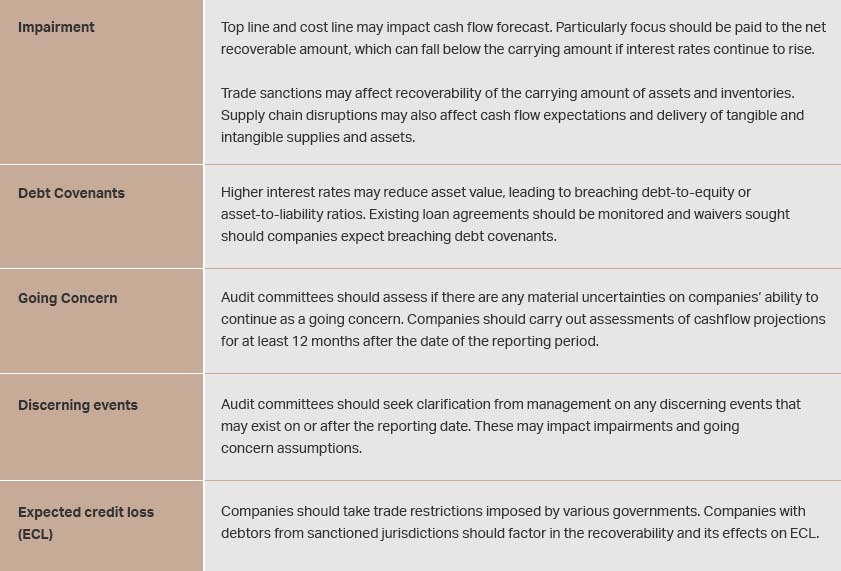

While Singapore’s core inflation eased as 2023 progressed, the macroeconomic outlook due to external events such as wars in Ukraine and the Middle East continue to be uncertain. Geopolitical uncertainties will continue to play a part in companies’ assessment of their business projections going forward. Such uncertainties may impact the following areas:

Climate Change Movement

The Singapore Exchange (SGX) has mandated that climate reporting be included for issuers with financial year commencing between 1 January to 31 December 2023 in the following industries: financial industry; agriculture, food and forest products industry; and energy industry. For financial year commencing between 1 January to 31 December 2024, it will be mandatory for issuers in the materials and buildings industry; and transportation industry. For all other issuers, climate reporting will remain on a “comply or explain” basis.

Singapore has implemented a carbon tax of $5 per tonne of carbon dioxide equivalent (tCo2e) until 2023. This tax will be progressively increased up to $80 per tCo2e by 2030. Audit committees and management should assess the impact of the climate-related risks and legislations on their operations, cash flows, and financial performance.

New accounting standards beginning 1 January 2024 have been implemented by ACRA and directors should be familiar with their adoption. Engaging accounting firms in Singapore to assist in the preparation of financial statements will reduce errors and omissions in disclosures related to the new standards. For fund companies preparing their FS for FY2023, engaging external auditors and an accounting firm with fund accounting and fund administration expertise early is encouraged.