Directors’ income in Singapore

Last updated on 31 March 2022

Directors of companies play an essential role in guiding the company in its business direction, management of the company and fiduciary duties. Accordingly, directors’ compensation varies in many forms, including salaries, directors’ fees, and stock options.

In general, directors’ compensation is taxable in the company’s country of incorporation or which it is a tax resident of. All monetary compensation to directors is taxable in Singapore, including allowances and benefits-in-kind such as club memberships under the director’s name paid for by the company. However, certain incomes are not taxable. Providers of HR and payroll services will be able to advise you which income type is taxable.

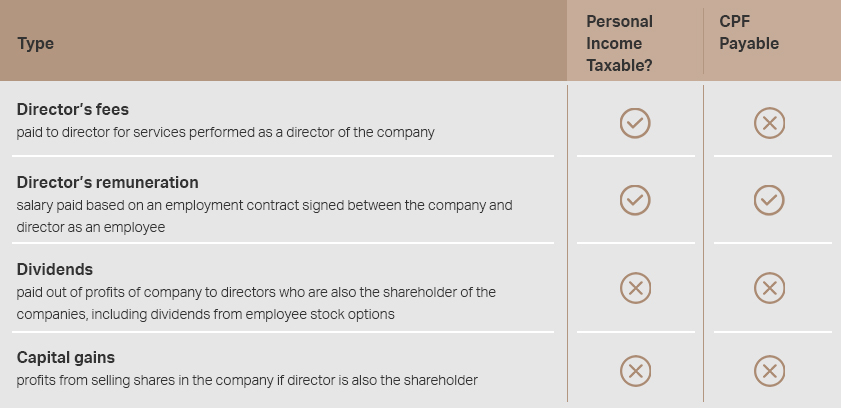

In Singapore, salaries paid to locally-resident directors (Singaporeans and permanent residents) are considered employment income and require Central Provident Fund (CPF) contribution. However, directors’ fees are not CPF payable. The table below explains what type of income is taxable and CPF payable.

All employment income and directors’ fees are to be included in the IR8A forms to be given to the directors by 1 March each year. This applies to resident directors – those who stayed more than 183 days in Singapore the previous year. For non-resident directors – those who resided less than 183 days in Singapore the previous year, companies are required to file and pay withholding tax for all remuneration to non-resident directors regardless of the amount paid. For more information about personal income tax click here.

For directors who are also a shareholder of the company, any dividends paid to them are not taxable as dividends are not considered employment income. Individuals who are unsure of the various types of taxable income can approach companies providing accounting services in Singapore that also offer personal income tax services to assist them in their tax filing.

Business owners who prefer to eliminate the confusion and headache of such payroll matters should consider the option to outsource HR payroll services to a payroll services provider. This will free up human and other resources to enable to company to focus on its core business.