Goods and Services Tax (GST) basics for businesses in Singapore

Last updated on 13 October 2021

GST is a tax on domestic consumption, collected for nearly all taxable supplies of goods and services in Singapore. It is also levied on goods imported, regardless of whether the importer is GST-registered, with the exceptions.

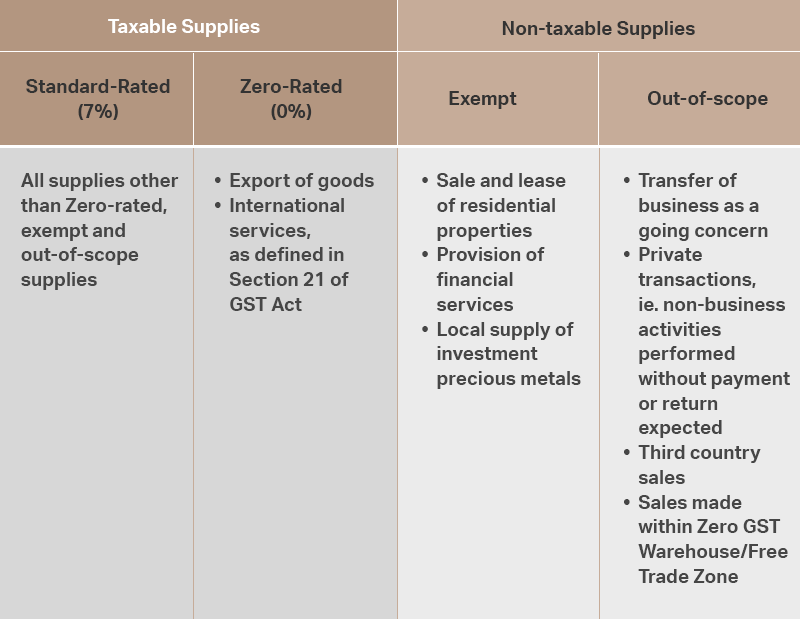

Supply is defined to include sale, transfer, exchange, barter, license, rental, lease and disposal. If a person undertakes either of these transactions during the course or furtherance of business for consideration, it will be covered under the meaning of Supply under GST.

The types of supply can be generalised as follows:

GST Registration

All businesses in Singapore with annual taxable supplies exceeding S$1 million are required to register for GST. Businesses that do not exceed S$1 million in taxable supplies may also voluntarily register for GST.

To qualify for voluntary registration, you must satisfy any of the following:

- Your business makes taxable supplies;

- Your business only makes out-of-scope supplies. Out-of-scope supplies mainly refer to sales of goods that did not enter Singapore and goods in transit;

- Your business makes exempt supplies of financial services that are also international services; or

- Your business procures services from overseas service providers and you would not be entitled to full input tax credit even if you were GST-registered.

With effect from 1 January 2020, GST registration requirements have been updated to cover businesses operating outside Singapore that are supplying digital services to consumers in Singapore. The registration requirements are further extended to non-digital services and low-valued goods imported via air or post, with effect from 1 January 2023. These extensions are meant to level the GST treatment between local and overseas vendors. More details on GST requirements for businesses operating outside Singapore would be covered in a subsequent blog.

It is advisable to consult professionals who provide GST services and accounting services in Singapore if you need assistance to determine whether your business should register for GST.

On-going compliance after GST registration

GST-registered businesses are required to charge and collect output tax on all taxable supplies, based on the values of supplies at the time of supply. If the supply is for a consideration wholly in money, the equation of the value of the supply is as follows:

Collected output taxes and the input taxes incurred on business purchases (including imports) and expenses, are reported to IRAS via the submission of GST return. For imports of goods into Singapore, the Singapore Customs administers the collection of GST according to the provisions of the Customs Act (Cap 70).

On the imports of goods, it is noteworthy that the point of transfer of ownership of imported goods to local customers would affect the determination of whether it is a standard-rated supply or, an out-of-scope supply. The named importer/consignee would also determine the party responsible for the input taxes at the point of import.

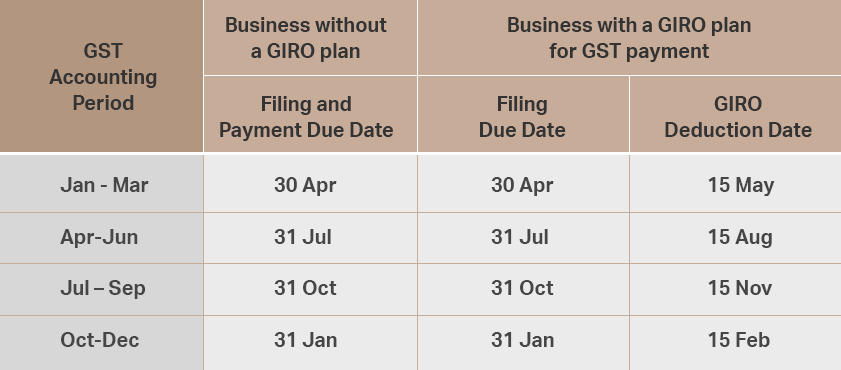

GST return is to be submitted within a month from the end of each prescribed accounting period, done usually on a quarterly basis. With the input taxes and output taxes recorded, the difference would represent the net GST that is payable to IRAS or refundable by IRAS.

The table below sets out the due dates for the submission of GST return for a typical GST-registered business.

The late submission penalty of $200 is imposed immediately once the GST return is not filed before the due date. A further penalty of $200 will continue to be imposed for every completed month that the GST F5/F8 return is outstanding, till the maximum of $10,000 for each outstanding F5/F8 return.

The content above is not meant to be a comprehensive guide on GST. To save yourself from being mired down with the compliance and details of the rules and regulations, you may wish to engage a company providing accounting services in Singapore and GST compilation services.