Employers required to provide employee income information by 1 March

Last updated on 24 February 2022

Operational & Process Excellence

Digital Capabilities and Performance Improvement

Other Business Support

Last updated on 24 February 2022

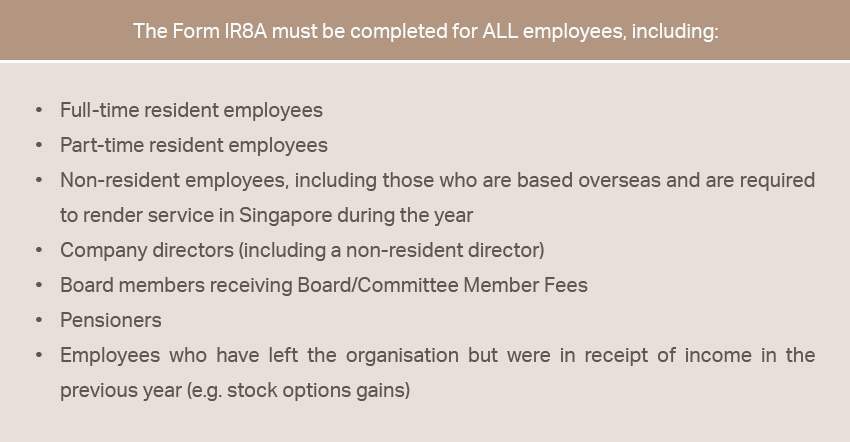

Under the Income Tax Act, all employers must submit employees’ income related information for all their employees for the purpose of their personal income tax returns by 1 March every year.

The Inland Revenue Authority of Singapore (IRAS) encourages employers to sign up for the Auto Inclusion Scheme (AIS). Employers under AIS need not prepare the hardcopy Form IR8A for their employees as the employment income information submitted will be reflected in the employees’ electronic tax returns. From the Year of Assessment 2022 (for income derived in 2021), it is compulsory for all employers with 5 or more employees to participate in AIS.

Form IR8A includes information on all salaries, benefits-in-kind and CPF contributions for each employee. Employers who are not under the AIS will have to provide the hardcopy Form IR8A and appendices to their employees by 1 March each year to file their personal income tax returns. The penalty for failure to comply may result in a fine not exceeding S$1,000 or a jail term in default of payment of the fine.

There are several appendices for Form IR8A as follows:

Due to the intricacies of completing the forms, many employers engage the services of companies that provide HR and Payroll services and accounting services in Singapore to help them prepare the Form IR8A or administer the AIS submissions to IRAS. This route is particularly economical for Small and Medium Enterprises that may not have in-house expertise for their accounting and bookkeeping needs.